For the second day, the market shook off early weakness and rose throughout the day. Today the markets closed at session highs. Volume levels rose on the

Nasdaq, making for back to back accumulation days.

Breadth was solid, and net new highs expanded. Investor sentiment remains skeptical, with the

ISE Index closing at the low level of 117. This indicates that many investors continue to fight this rally. At some point, performance anxiety could kick in and exacerbate things on the upside.

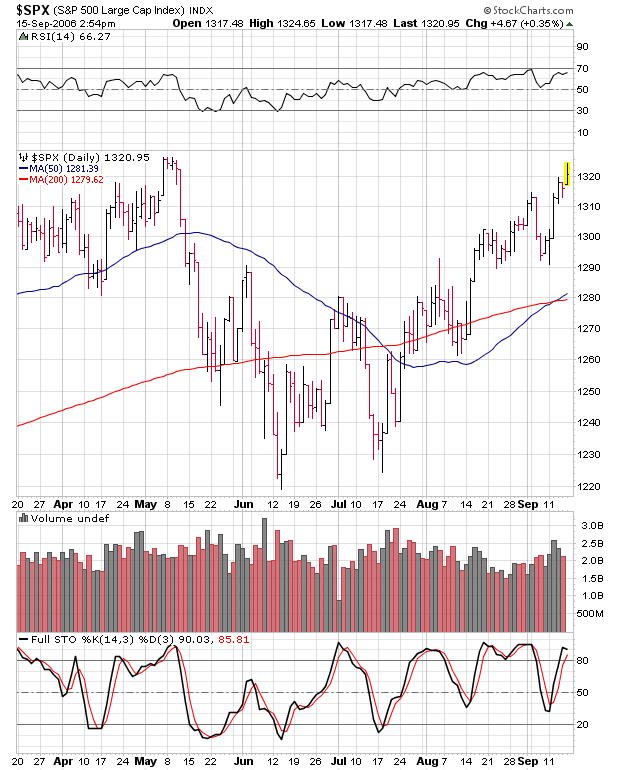

As the chart above shows, the

COMP has been lagging its larger

SPX bretheren, and is now trying to play catch-up. The growth stock index has broken above its 200-day moving average, which it successfully tested yesterday. Bulls want to see this former resistance area coverted to solid support in the near future.

As for the SPX, it closed at another yearly high (1336). The last time the SPX was at these levels was February 2001.

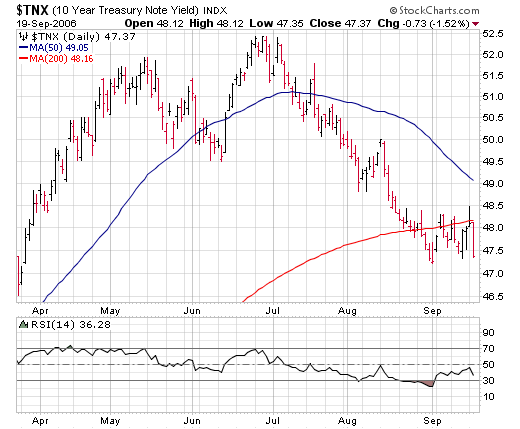

Oil closed flat around $61.25, while bond yields finally rose, with the

10-year closing at 4.58%.

After the close,

RHAT reported earnings, but the stock fell sharply as investors were disappointed.