Who Says September Is The Worst Month For Stocks?

The markets finished slightly lower on the day, despite being up sharply in early trading. Stocks got off to a strong start after the opening bell this morning, when the final revision to Q2 GDP showed that the economy grew 1.7%, from an earlier estimate of 1.6%, due to stronger than expected consumption.

Also, weekly jobless claims came in below expectations, and the Chicago PMI survey rose to 60.4, much better than the 56.0 expected. The various PMI reports have been somewhat weak lately, so this strong reading emboldened buyers.

There was no real news that accounted for the selloff, but within the first half hour of trading, stock prices peaked and the market began to selloff. Nonetheless, the S&P 500 finished the month of September with a gain of roughly +8.8%. The final figures aren't in, but I have heard that this was the best month of September since 1939 - quite a showing.

It's funny, because many market spectators were worried about September, as it has a history of being the weakest month of the year for stocks. But with a big down August this year, we had been saying that all of the negative stories were already well know and thus likely discounted in stock prices. Stocks ramped higher on the first day of the month, and pretty much added to those gains each week thereafter.

The dollar was flat today, although it has been weak this past month. That helped gold prices rally in September, finishing the month at $1308.

The 10-year yield rose slightly to 2.51%; the volatility index crept +2% higher to 23.70, right at its overhead 50-day average.

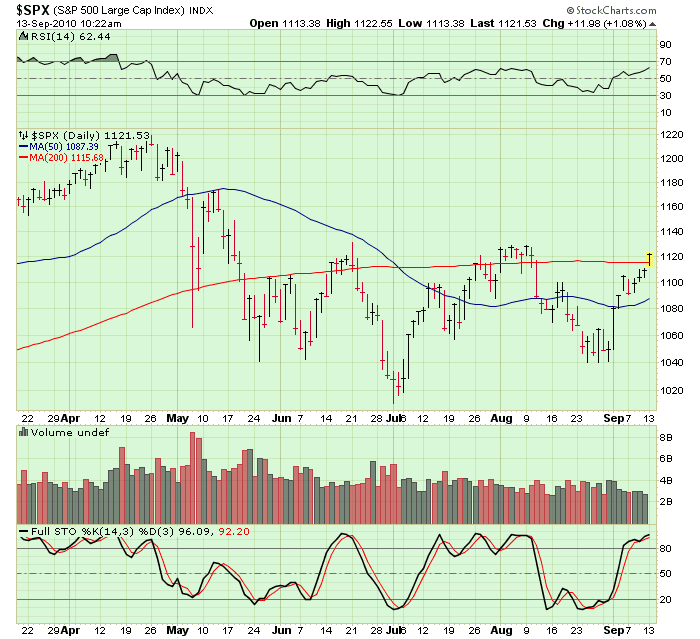

Trading comment: Given the sharp runup over the last month, most are expecting some sort of pullback over the next week. But given that it seems many portfolio managers are underinvested and in dip buying mode, it will be interesting to see at what levels buyers step up to the plate.

I'm still keying off of SPX 1131 as initial support, and then 1115. The 50-day average is currently at 1104.

posted by J. Kahn @ 1:11 PM

0 comments

![]()

![]()