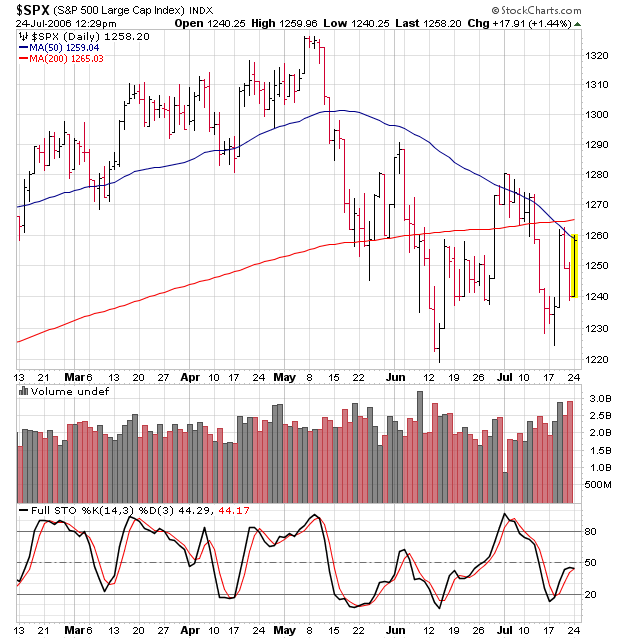

The stock market was schizophrenic this week. It loved the

Fed, it hated the Fed. It loved the earnings reports, it hated the earnings reports. Not surprisingly, the indices ended mixed for the week. Ultimately though, the fundamentals improved.

The market opened the week with a mixed day on Monday. The

S&P lost 2 points, but the Nasdaq and Dow were up. The market was looking forward to the

PPI and

CPI data later in the week and the flood of earnings reports that would start after the close on Monday. Good earnings news before the open from

Citigroup and

Harley-Davidson had little broad impact.

Tuesday was another day of a holding pattern. The S&P regained the 2 points it had lost the day before. The June

core PPI came in at a comfortable 0.2%. That was in line with expectations and did not cause concern. Earnings reports were generally good.

Coca-Cola, Johnson & Johnson, and

United Technologies in particular posted good numbers.

Wednesday the market busted loosed. Before the open, the June

core CPI was reported to have jumped 0.3% for the fourth straight month. The year-over-year increase rose to 2.6%. The data raised inflation concerns and the S&P futures dropped sharply. The conclusion was that the Fed would probably have to raise rates again in August to counter building inflationary pressures. Fed funds futures priced in a high probability of a rate hike.

Then

Bernanke testified before Congress at 10:00 ET. His testimony turned that logic on its head. Bernanke said that the

core personal consumption (PCE) deflator, which does not include the rental equivalency measure for housing costs, was a better measure of inflation than the core CPI. It has been up 0.2% each of the past two months and the year-over-year gain is only at 1.9%.

Furthermore, Bernanke indicated that the Fed expects core inflation to ease in 2007. That implies the Fed might be willing to wait for the impact of the previous rate hikes to take effect, and not feel the need to raise rates right now.

Fed funds futures plunged as expectations of an August rate hike dropped sharply.

Bernanke clearly indicated a more dovish stance towards policy and the 23 point surge in the S&P 500 index that day was justified on that basis.

Earnings reports also helped, as

IBM, JP Morgan, Bank of America, and

UnitedHealth Group posted good numbers.

Yahoo, however, gave a soft outlook and the stock was hit.

Thursday, the market shifted personality again. The release of the June FOMC minutes did not reflect as dovish a stance as Bernanke had done the day before. The market became concerned that the Fed might indeed raise rates in August. It is not clear why the market would place so much emphasis on minutes that are now many weeks old when the Fed Chairman had spoken on policy the day before. Nevertheless, the market was near flat at mid-day but sold off after the release of the minutes to end with an 11 point loss on the S&P 500 index.

Also hurting the

Nasdaq that day was a disappointing report and outlook from

Intel. A

pple and

Motorola had excellent reports, but Intel's numbers were more influential.

Friday the S&P 500 lost another 9 points. A major factor was a warning from

Dell that second quarter profits would be lower than expected. There was probably also some risk-event selling ahead of the weekend given the continuing conflict in the Middle East. As to the Fed outlook, fed funds futures ended the day with a 45% chance of a rate hike at the August meeting built into the price structure.

Earnings overall this week were good. The best numbers came from Dow firms such as Coca-Cola, Citigroup, Caterpillar, Honeywell, IBM, JP Morgan Chase, Johnson & Johnson, and United Technologies. Even Pfizer posted good numbers. As a result, the Dow had a strong week and advanced 1.2%.

There was far greater concern in the tech sector. Intel, Dell, and Yahoo gave cautious to poor outlooks. These key companies overrode the impact from good earnings from some companies such as Apple and Google. The broader technology picture is of concern, while some companies remain in growth mode. The Nasdaq took it on the chin again this week.

Overall, however, the market enters the latter stage of earnings season on a sounder footing. There is no reason to doubt the veracity of Bernanke's testimony. He clearly represented a less hawkish stance than the market had assumed at the start of the week. Earnings are coming in better than expected (as usual) and warnings are far less prevalent than feared. Economic growth is clearly slowing, so many companies will have trouble posting good earnings numbers the second half of the year. That should not be surprising.

The near-term outlook remains mixed, and perhaps even dicey for the tech sector, but the longer-term outlook is improving. The market is coming to grips with the reality that earnings growth will have to slow down in the quarters ahead. The end of the rate hike cycle is clearly nearing. And valuation measures have improved significantly.

The crisis in the Middle East remains an important wild card, but at least oil prices came off their highs to end near $74 a barrel. The market faces another week of heavy earnings reports, and individual companies that warn will get slammed. The foundations for a year-end rally, however, may be falling into place.

-- Briefing.com